Lucky Strike Entertainment (LUCK): Q2 Thoughts & Outlook

Boy Do They Need Some LUCK

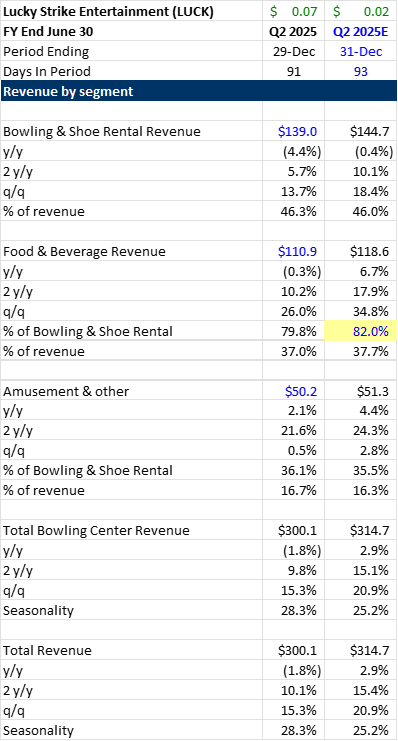

Q2 Results Should Be (Another) Thesis-Breaking Quarter for Longs

In their seasonally second-strongest quarter of the year, they faltered. Same-store sales (SSS) declined 6.2% (vs. guidance of approximately flat), and management commentary/tone suggests a low single-digit (LSD) decline for the full year. While expectations coming into the quarter were low, estimates are moving lower. The stock remains expensive despite a relatively strong macroeconomic environment. Additionally, due to its fixed cost base and leverage profile, there is an almost 100% probability that the company will face a liquidity issue within the next decade.

Same-center revenue declined 6.2%, the worst result since the pandemic. I estimate pricing increased 3.3% year-over-year (y/y) and 1.3% quarter-over-quarter (q/q), while traffic fell 10% y/y. Management reported flat retail traffic, but corporate and event traffic underperformed:

*"Event business was down mid-single digits in the quarter… Offline events, which include corporate events and office parties, are a major driver in December. In October, we saw a lot of election uncertainty. By December, while customers who had planned six months out followed through with their bookings, last-minute parties simply didn't happen. From our perspective, events—or what we call offline events—represent 25% of our Q2 business, but that drops to about *13% for the rest of the year."

Promotions & Strategic Shifts

The company has been highly promotional, offering 50% off a third game, a pizza & pitcher deal, and other Groupon offers. In its short time as a public company, the number of strategic shifts has been striking. It started with the Money Bowl app to drive traffic, then pivoted to promotions encouraging customers to bowl a third game, and now focuses on premium food & beverage (F&B) offerings and rebranding locations to Lucky Strike.

Interestingly, management promotes bowling as an affordable activity—suggesting that consumers trade down for cheaper entertainment—yet all recent actions aim to increase prices and position the business as a more premium form of entertainment. The Q2 call referenced initiatives such as coat check services and a new events menu, reinforcing this premium push. I estimate the average customer spends ~$47.40 per visit, increasing to ~$55 with tips.

New Openings & Expense Management

During the quarter, the company opened four new Lucky Strike locations and acquired Boomers Parks & Spectrum Entertainment Complex for $42.8m. Early performance at Lucky Strike Beverly Hills and Lucky Strike Ladera Ranch has been promising, generating over $1m in revenue in their first month.

A notable positive in the quarter was expense management, particularly in labor costs. Labor costs per center declined 12% y/y, reflecting improved efficiency. Handheld tablets increased server capacity, allowing staff to cover more lanes, reducing center costs, and improving four-wall margins.

Outlook & Revised Q3 Expectations

Management estimated that wildfires in Los Angeles caused a $5m revenue impact, offset by the school winter break shift from Q2 to Q3. January comps are down LSD, but February and March are expected to improve.

A $5m impact on a $330m quarter equates to a ~1.5% headwind, making comps roughly flat when backing out the fire impact but giving them benefit for the calendar shift. In addition, Q3 FY24 comps of -2.1% make comparisons easier.

If January comps are flat, February and March could be down LSD, putting total comps at ~ -3%. However, I believe this is overly punitive, and I expect comps to turn positive.

Before today's results, I projected Q3 FY25 comps of +8.1%, driven by improved F&B offerings and calendar shift benefits. My revised Q3 revenue estimate is $350.4m, reflecting +1% SSS growth and new center openings.

Despite a challenging Q2 and a slow Q3 start, management reiterated FY25 revenue guidance of $1.25B and $410m in adjusted EBITDA. I expect guidance to be revised downward in Q3 due to continued business underperformance. The cynic in me wonders if the summer-related acquisitions are partly done to boost May-June results and meet targets.

Catalyst Watch

Negative: Potential write-off of net operating losses (NOLs) due to a lack of visibility on future utilization.

Negative: Wall Street is still bullish on the stock; however, JP Morgan downgraded the stock ahead of earnings. Additional downgrades pressure the stock.

Positive: A rebound in corporate events could drive upside to estimates.

Positive: Rebranding 70 Bowlero/AMF centers to Lucky Strike could accelerate SSS growth.

Final Thoughts

Estimates are declining, and business is underperforming.

Expense management is a notable positive, and continued cost discipline is critical to maintaining margins amid weak corporate event spending.

Corporate event recovery is a key metric to watch. If demand fails to normalize, it may indicate that normalized corporate spending is lower than recent historical trends.

The stock remains expensive and unattractive at current levels.