Franklin Covey

Cheap With Accelerating Fundamentals

Date - 8/9/24

Company – Franklin Covey

Ticker – FC

Stock Price - $38.91

Market Cap - $509m

EV - $481m

Fiscal Year Ends – 8/31 (Years referenced below relate to Fiscal Year)

Summary

Franklin Covey’s (FC) FY2H 2023 and FY1H 2024 were relatively disappointing. Headline risk about an imminent recession caused businesses to pull back on discretionary spending. Q4 23-Q2 24 revenues declined y/y, with the most recent quarter (FQ3) returning to growth. Easy comparisons, growing deferred revenue, share repurchases, and new sales hires fully ramped present a compelling setup. The one-sentence thesis is – that numbers are too low, and the stock is cheap; looking out a few years, buyback accelerates the rerating.

Business Description

Franklin Covey is a global consulting and training leader specializing in performance improvement, helping organizations achieve results that require lasting changes in human behavior. Their offerings are designed to help clients increase their efficiency, productivity, and effectiveness through proven practices and principles.

Mission

1. Develop exceptional leaders at every level.

2. Instill habits of effectiveness in every individual.

3. Build an inclusive, high-trust culture.

4. Use a common execution framework to pursue their most important goals.

Training Programs—Develop skills to lead an organization. Productivity classes improve efficiency through effective time management and organizational skills. Sales performance enhances selling practices. Organizations have employees with significantly different skill sets, work environments, and demographics. Franklin Covey provides training so managers can have more meaningful conversations with employees.

Consulting (Over 250 senior-level consultants on staff): Provides customized services to help organizations implement the principles and practices of Franklin Covey's training programs. These include coaching and mentorship programs, organization assessments to understand an organization's state, and leadership diagnostics, which help leaders identify strengths and weaknesses in their ability to manage an organization.

Books & Publications – They have numerous best-selling books, including "The 7 Habits of Highly Effective People", “Trust & Inspire,” and “The 4 Disciplines of Execution.” These books serve as foundational texts for their training programs and principles.

Customers include – Corporations, Government Agencies, Education Institutions, and other small and medium-sized enterprises. Notable customers include Proctor & Gamble, United Health, Pepsi, and Marriott.

Revenue Segments

Enterprise Division – Includes Direct office and International license.

Direct Office - Clients in the United States and Canada; international offices that serve clients in Japan, China, the United Kingdom, Ireland, Australia, New Zealand, Germany, Switzerland, and Austria; and other groups such as government services office and books and audio sales. Primary Product – All Access Pass

International License - In foreign locations where they do not have a directly owned office, training and consulting services are delivered through independent licensees.

Education - Domestic and international education practice operations are focused on sales to educational institutions. Primary Product - Leader in Me program.

Corporate & Eliminations - Royalty revenue from Franklin Planner Corporation, leasing operations, shipping and handling revenues, and certain corporate administrative expenses.

Background

Franklin Covey’s transition to the All Access Pass(AAP), away from its traditional business model of selling content and solutions one course, or one solution at a time, and often to only one team through one modality at a time. AAP was announced in early 2016 and rolled out with targeted availability to clients while adding new solutions and functionality to its web portal. With an All Access Pass subscription, pass holders can assemble, integrate, and deliver Franklin Covey’s individual and leadership development content in an almost limitless combination through various delivery channels — live, live-online, on-demand, and incorporated into existing training offerings.

Passholders also have exclusive access to an implementation specialist — an expert in Franklin Covey’s solutions — and other services to ensure they are unleashing the full scope and power of the All Access Pass to achieve their business objectives. Franklin Covey’s All Access Pass uses a cost-per-population model, which lowers the cost barrier and creates a strong value proposition for clients while increasing the flexibility and availability of learning to their teams and organizations. Passholders also receive special pricing on books, on-site consulting, custom solution design, and facilitator and participant materials.

Integrating the program throughout an organization, not on a one-off basis, improves client retention, revenue visibility, and addressable market. All Access Pass increases the average client sales size, improves cross-selling opportunities, and helps clients realize more value through access to expanded content and purchase additional services and training materials. All Access Pass continues to comprise more sales, up from 31% in 2020 to 35% in 2023, increasing YTD in 2024. Since the All Access Pass launch, gross margins increased 1000bps from 66.1% in 2017 to 76.1% in 2023. This pricing power displays the value customers place on these products.

Thesis

Q4 2023 – Q2 2024 results underperformed expectations. Clients pulled back or delayed spending due to macroeconomic concerns. Revenue growth decelerated substantially from 8% in Q3 23 to -1.1% in Q4 23, -1.4% in Q1 24, and -0.7% in Q2 24. Q3 24 improved to +2.7%, a positive sign that corporations, school systems, and the government began spending again. Despite the revenue decline, gross margins were flat in these quarters, while Adj. EBITDA margins declined in Q1 & Q2 24, expanding in Q3. The SASS-like business model creates a high incremental margin business model. As shown below, incremental margins differ for each segment, with international licenses having the highest (unsurprising as there’s almost no added cost with a licensed product). Direct Office incrementals of ~80% normalized, followed by education at 65%.

Due to the poor performance over the past year, comparisons entering Q4 24 and into 2025 are relatively easy. Deferred revenue is up 8.7% y/y in Q3. Deferred revenue is a good proxy for future revenue growth, as the multi-year all-access pass contracts generate revenue in coming quarters. With 80% incremental gross margins, the increased revenue significantly impacts EBITDA generation.

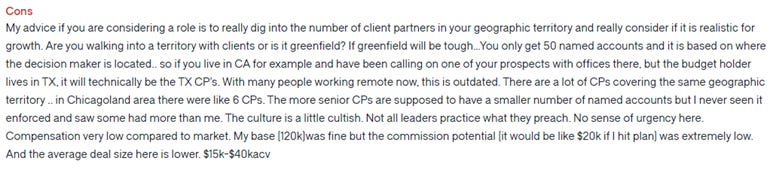

From 2012 - 2022, client partners(sales force) grew by 250% from 120 to 300 client partners. Of these additions, at least 1/3 have occurred between 2018-2022, many of whom are in the early stages of that ramp. In 2024, this figure declined to 265. The decline stemmed from people who didn’t fit within the planned future field deployment structure. In Q3 24, they hired four partners and expect to ramp hiring into 2025. Their new go-to-market project, “speed-to-ramp,” is designed to sell products and services to new organizations. They are targeting ~400 client partners over the next several years, which should lead to incremental sales growth as these employees fully ramp up. One concern is the available territory for new hires. Many client partner employee reviews stated they had little opportunity to make new sales as territories already had dedicated partners. If they continue to bump against the 300 mark and fail to grow beyond this, I will be increasingly worried their client count has peaked.

The capital-light business model and high incremental underscore the potential EBITDA uplift as revenue grows. Net Income is a good proxy for Free Cash Flow generation as capex is negligible. Management has been aggressive lately with capital deployment. With $36m of net cash and an estimated ~$10m generated in Q4, I expect buybacks to continue. They’ve repurchased 649k shares worth $25.8m, $7.4m/188k in Q3, and currently have a $50m repurchase authorization. These buybacks are currently accretive to the business and provide a re-rating tailwind.

I estimate revenues will increase by 12.8% in 2025 due to a 5% growth in deferred revenue in 2024 and new business wins. Edition 5.0 of the 7 Habits will be released in the fall. It's been 9 years since the last update, and I anticipate this will drive incremental sales. Since the initial release, over 40 million copies have been sold.

Revenue growth will drive the stock and business. They’ve proven the SASS-like business model and the high-margin service offering. Estimates heading into 2025 are too low, with consensus revenue and adj. EBITDA of $305m and $60m vs. my estimate of $321m and $72.4m.

The upside is that no one believes management will hit their Q4 and FY guide (including myself), even though they reiterated Q4 guidance of $80.5m (attainable) while they expect Adj. EBITDA to come in at $54m for the entire year (~$22m in Q4). This would put EBITDA margins at 27.3%, or a 680bps improvement on Q4 23’s results. This is a stretch; however, given they reported at the end of June and Q4 ends in August, they must have visibility into the pipeline and cost structure that gives them the confidence to reiterate this. Note Q4 23’s 20.5% EBITDA margins were the highest in the company's history. To think they will beat this by 680bps either means they are sandbagging revenue guidance or lower client partner headcount drives this incremental margin improvement. I expect them to come ahead of their revenue guide should they have any chance of hitting the FY EBITDA target. The important part is that this marks a notable acceleration in the business, which management expects to continue into 2025.

While sell-side estimates (four smaller sell-side firms cover the name) take the guidance at face value, the buy-side bogey is also below guidance. Otherwise, this stock would not trade where it does today. Q3 24 EBITDA y/y growth accelerated to +17% y/y compared to -9% in Q2. If management hits its guidance, EBITDA growth accelerates to +32% y/y. This growth algorithm would warrant an EV/TTM EBITDA greater than 10x. Expectations are low, as 2024 in general has disappointed. In 2025, I expect EBITDA growth momentum to continue, as the high incremental margins combined with accelerating revenue growth drive 40%+ EBITDA growth, compared to the street's 12% growth. The hiring and productivity ramp of new client partners determines the result.

Project penetration is relatively new; however, it has shown success. Q2 24 Call: “Under the direction of the client partner, Impact Pods' sole focus has been to help clients achieve such great results that we would earn the right to expand our solutions even further.” Pods are tasked with ensuring clients get the most out of their subscriptions. Corporations are unlikely to cancel a subscription if employees are benefiting in a significant way. By increasing the value clients place on Franklin Covey resources, they are more likely to add on additional services. The incremental revenue opportunity is substantial as FC is only 10%-15% penetrated with this model.

In the end, business is improving; several initiatives are underway to drive incremental growth, which, combined with high incremental margins, accelerates EBITDA and EPS growth.

30-year Reverse DCF Assumptions

Using a relatively simple Reverse DCF, where revenue through 2026 aligns with my base case, after that, declining to 2% growth in 2027 thereafter. Incremental EBITDA margins of 25% are well below what I believe is the normalized figure. Note, revenue for All-Access Pass per client has grown at Mid to High single digits over the past 3 years, making it unlikely revenue will decline to GDP growth—additionally, incremental Adj. EBITDA margins have been volatile, though they have generally been between 20%-45%.

Risks

We contacted Franklin Covey for internal purposes to see if they could help our organization. After being contacted initially to set up a call, there was no follow-up. We were told a rep would contact us, but one did not. This poses a significant risk of potential sales opportunities falling through the cracks.

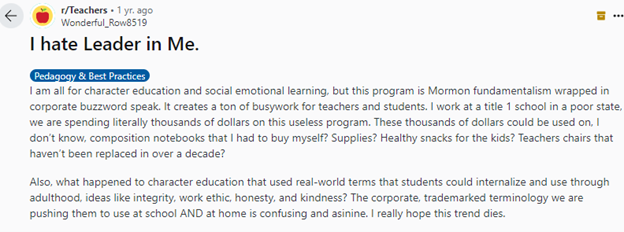

Reviews online of the Leader in Me program are concerning (see below). While any product will have positives and negatives, getting teachers on board and buying into the program is critical to its success. Should enough teachers state the program is unhelpful, schools would pivot.

https://www.reddit.com/r/Teachers/comments/15h2ucd/i_hate_leader_in_me/

A review of employees at the company relates to micromanagement, lack of growth opportunities, and being behind in technology. It is concerning that technology-based companies may lack the necessary internal tools to generate sales, though reviews are skewed positively. I worry the long tenure of board and management members has resulted in complacency and a lack of innovation. Robert Whitman (chairman) has been chairman since 1999. Paul Walker, the CEO, has been with Franklin since 2000. Although relatively young at 48, he has led the All Access Pass transition efforts. Stephen Young, CFO since 2001.

Go Forward KPI’s

- Client partner hires

- All-access pass subscription revenue and invoiced amount

- Deferred Revenue

- Percentage of All Access Pass subscriptions on multi-year contracts