Compass Minerals (Ticker:CMP)

New Management Initiatives + Strong Q2 Should Drive The Stock Higher

Company – Compass Minerals

Ticker – CMP

Date – 3/29/25

Stock Price - $9.58

Market Cap – $397m

EV - $1.326B

FY End – 9/30

Disclosure - O’Keefe Stevens Advisory has a position in Compass Minerals (CMP).

Summary

Back to Basics will drive shareholder value. Distractions, operational challenges, missed filing deadlines, and misallocated capital resulted in substantial shareholder value destruction over the past several years. In January 2024, Edward Dowling was appointed as the new CEO, succeeding Kevin Crutchfield, who has held the position since May 2019. Under Kevin’s leadership, CMP’s stock declined by 57% (excluding dividends, which was cut in February 2024) due to poor capital allocation decisions, which are now being addressed by the new management team. With these distractions removed and focus restored to its core Salt operations, free cash flow generation will enable the company to reduce and refinance its debt. As leverage concerns ease, earnings inflect higher after a mild FY2024 winter and little precipitation in FQ1; the high-quality assets Compass owns will be drive higher earnings power.

Thesis

- Market is missing the $50m contract signed with Buffalo. In addition, investors are completely offside and are mismodeling normalized earnings power.

- Cost-cutting initiatives will improve margins as they exit their loss-making retardant business. Should the sulfate of potash (SOP) market remain soft, management may choose to exit this business, eliminating another loss-making business (simplifying the story even further).

- Historically poor free cash flow conversion improves due to lower capex.

- Working capital release will enable them to generate significant FCF, which can be used to pay down upcoming maturities.

Risks

- A weak pricing environment from mild winters has depressed salt pricing and volumes.

- Several misguided business initiatives resulted in significant capital destruction.

- A new, lower-cost salt mine is expected to come online in 2030, which could pressure pricing.

- The plant nutrition (SOP) market is experiencing weak prices, resulting in operating losses.

Business Overview

Compass Minerals is a leading producer of essential minerals, primarily focusing on salt and specialty plant nutrients. The company operates through two key business segments: Salt and Plant Nutrition (sulfate of potash). Compass Minerals has built a broad geographic footprint within these segments, with major production assets in North America and a presence in the United Kingdom and Brazil. This diversified asset base and product mix position the company as a critical supplier in its markets, serving customers ranging from municipal road agencies to agricultural growers.

Salt Segment: Accounting for 83% of the 2024 revenue. Producer of highway deicing salt, industrial salts, and consumer salts (such as table salt, water-softening pellets, and ice melt products). Their Goderich salt mine in Ontario, Canada, is the largest underground salt mine in the world. Goderich has an annual production capacity of up to 9m tons and is located on the shores of Lake Huron, enabling low-cost shipping via the Great Lakes to key markets in the U.S. and Canada. Their Cote Blanche mine in Louisiana has an annual production capacity of 3.4m tons. Cote Blanche serves the U.S. Gulf Coast and Midwest markets, with access to barge transportation on the Mississippi River system. Buffalo, Chicago, Cincinnati, Cleveland, Detroit, Milwaukee, Minneapolis, Pittsburgh, St. Louis, Montreal, and Toronto are the 11 primary markets Compass serves. Additionally, they operate a rock salt mine in Winsford, United Kingdom (Cheshire), to supply deicing salt to the U.K. market. Beyond these rock salt mines, Compass Minerals produces refined evaporated salt at Kansas, Saskatchewan, and Nova Scotia facilities. The company also manages an extensive network of storage depots and distribution points to ensure timely customer delivery. Customers include state and provincial transportation departments, municipalities, contractors, as well as industrial and consumer buyers, solidifying its market positioning as one of North America’s top salt suppliers.

Plant Nutrition Segment: The Plant Nutrition business focuses on high-value specialty fertilizers, primarily sulfate of potash (SOP). SOP is a potassium-rich fertilizer prized for its low-chloride content, which makes it ideal for sensitive crops such as fruits, vegetables, and nuts. Compass Minerals is the largest SOP producer in the Western Hemisphere. Its flagship operation is the solar evaporation facility at the Great Salt Lake in Utah, where the company harvests minerals from naturally occurring brine. At this site, Compass produces SOP under the Protassium+® brand with an annual capacity of approximately 350,000 tons. The Great Salt Lake facility also yields significant volumes of salt (around 1.5m tons capacity) and magnesium chloride as co-products. The Plant Nutrition segment once included a broader portfolio of micronutrients and specialty plant supplements, including operations in Brazil; however, in recent years, Compass Minerals has narrowed its focus. The company divested its micronutrient businesses by 2021 to streamline operations, and today, the segment is centered on SOP production and distribution. Compass markets its fertilizer products globally, selling SOP across North America (with an emphasis on the Western and Southeastern U.S. agricultural markets) and exporting to Latin America, Asia, and Oceania. Plant Nutrition represented 17% of 2024 revenue.

Historical Mistakes and Strategic Missteps

Previous management made several mistakes in the past decade, including a failed attempt to enter the lithium market, an ill-fated acquisition of a fire retardant business, and a major disruption at its flagship salt mine.

Aborted Lithium Development Initiative: In 2021–2022, Compass Minerals launched an ambitious plan to diversify into lithium production to capitalize on the booming demand for electric vehicle battery materials. The company identified significant lithium resources in the brine of its Great Salt Lake operations and announced plans to extract lithium carbonate equivalent (LCE) as a new revenue stream. Management touted this as a transformational opportunity and even secured a supply agreement with Ford for future lithium output. However, this initiative proved overly ambitious and encountered significant hurdles. In 2023, the project was indefinitely suspended due to intense regulatory and environmental scrutiny in Utah. State regulators raised concerns that large-scale lithium extraction could accelerate the depletion of the already-shrinking Great Salt Lake and negatively impact its ecosystem. New legislation in Utah imposed strict requirements on water usage and brine extraction, effectively stalling Compass’s project.

Fortress Fire Retardant Acquisition and Recent Shutdown: Compass Minerals ventured into the wildfire management sector with its investment in Fortress North America, a startup specializing in next-generation fire retardant chemicals. The rationale was to leverage Compass’s mineral expertise, as magnesium chloride and other salts can be ingredients in fire retardants, and enter a growing market for wildfire suppression products. Perimeter Solutions (Ticker: PMS) is the leading player in this market. Beginning in 2020, Compass took a minority stake in Fortress, and in May 2023, the company acquired full ownership (the remaining 55% equity) in a deal that brought total investment in Fortress to roughly $100m. Fortress developed a long-term fire retardant aimed at competing with the market leader in aerial firefighting chemicals. However, gaining regulatory approvals and customer adoption, primarily from the U.S. Forest Service and state wildfire agencies, proved difficult and time-consuming and was a drag on earnings. In March 2025, they announced the shuttering of Fortress and will lay off all associated employees. They estimate a savings of $11m-$13m from these actions. At the end of Q1 2025, they had $7.9m of contingent considerations associated with an earn-out. This should be eliminated due to the business's closure. The total impairment in Q2 results should be ~$56.5m from net intangible assets consisting of customer relationships, trade name, and R&D of $54.1m, $0.1, and $2.2m, respectively.

Goderich Mine Ceiling Collapse and Operational Disruption: Compass’s most important asset, the Goderich rock salt mine, experienced a serious operational setback in September 2017. A partial ceiling collapse occurred deep in the mine due to unexpected geological movement. Thankfully, there were no fatalities; however, the incident necessitated an immediate slowdown in mining rates for safety and remediation purposes. Production at Goderich was significantly constrained for many months as the company secured the affected area and re-evaluated its mining methods. This had a notable financial and commercial impact: during the winter of 2017–2018, Compass Minerals had to ration salt from Goderich and even invoke force majeure on some supply contracts. To keep key customers supplied, the company rerouted salt from its Louisiana mine to the Great Lakes region, incurring significantly higher transportation costs. Logistics expenses spiked, and overall salt segment costs in early 2018 were about $20m higher than usual, largely due to this contingency plan. The ceiling collapse not only hurt earnings but also tested Compass’s reputation for reliability. Some customers in the Great Lakes region experienced delays or had to source salt from competitors that winter. Compass took steps to prevent such issues going forward – including accelerating the transition of Goderich from traditional drill-and-blast mining to continuous mining machines, which improve safety and efficiency. By mid-2019, the mine was largely back to full capacity with modernized operations. Nonetheless, the 2017 collapse incident stands out as a costly mistake in terms of risk management.

Market Share & Competition

Compass Minerals operates in a competitive landscape, particularly in the salt industry. In North America’s salt market, a handful of large players dominate production and distribution, with Compass being one of the leading suppliers of highway deicing salt. The company’s closest competitors include Stone Canyon Industries (which owns Morton Salt and related operations), Cargill, and American Rock Salt, among others. Each competitor has its own production assets and logistical strengths, influencing regional market share dynamics.

The highway deicing salt market in North America is mature, has relatively low margins, and is heavily influenced by winter weather patterns. Total demand can vary significantly from year to year, depending on snowfall. Compass Minerals has historically been either the largest or second-largest producer of deicing salt in the region. The title of largest salt producer has often been associated with Morton Salt, a company with iconic brand recognition (the “Morton Salt Girl”) and extensive operations, which is now under the umbrella of Stone Canyon Industries. In 2020, Stone Canyon acquired Morton Salt (and its Canadian affiliate, Windsor Salt) from its German parent, K+S, instantly making Stone Canyon a major force in the industry. This acquisition, along with Stone Canyon’s prior purchase of the Kissner Group (owner of the Detroit Salt Co. mine and other assets), consolidated a significant portion of North American salt capacity under one private holding company. Compass Minerals, therefore, faces a much better-capitalized and larger competitor in Stone Canyon/Morton. Meanwhile, Cargill has long been a significant salt producer as part of its diversified agricultural commodities business, operating key mines and serving both deicing and industrial salt markets. American Rock Salt (ARS) is a privately-held company that runs a single large mine in upstate New York and focuses on serving the northeastern U.S. deicing market. Together, these companies account for the bulk of domestic salt production. Additionally, imported salt (from countries such as Chile, Mexico, Egypt, and the Bahamas) plays a significant role in coastal markets. During periods of shortage, it effectively acts as an alternative source of competition and price pressure.

In the U.S. Northeast, American Rock Salt has local transportation advantages. ARS’s Hampton Corners mine near Mt. Morris, NY is the largest operating salt mine in the United States by output, and it supplies a significant portion of road salt for New York state, New England, and parts of the Mid-Atlantic. ARS uses a dedicated rail to ship salt in bulk to regional depots and directly to some large customers, enabling it to compete effectively on logistics in the Northeast corridor. Stone Canyon (Morton/Windsor) also serves the Northeast through its Canadian mines in Nova Scotia (Pugwash) and Quebec (Mines Seleine on the Magdalen Islands), which ship salt via ocean vessels to eastern ports in Canada and sometimes the U.S. Moreover, Morton’s solar salt facility in the Bahamas, located on Great Inagua, produces over a million tons annually. It can dispatch vessels to East Coast U.S. ports, such as Newark, Boston, and Baltimore, when needed, providing an additional source of supply in the Northeast. Compass Minerals, on the other hand, has less direct presence in the far Northeast. It can indirectly supply some customers in the region — for instance, by sending Goderich salt through the St. Lawrence Seaway or by rail or truck from Great Lakes stockpiles — but it has historically not been the dominant player. Thus, in the Northeast, ARS and Stone Canyon’s network generally set the competitive tone, with imports filling any gaps in severe winters.

Due to the weight and low unit value of salt, logistics are often the deciding factor in competition rather than pure production volume. Each competitor has carved out certain logistic advantages (as outlined in the table), meaning Compass must continue to optimize its transportation, whether via ship, barge, rail, or truck, to maintain healthy margins and market share.

Overall, Compass Minerals’ competitive outlook in the salt segment is that of a major player in a fragmented but consolidating market. Its strengths lie in its high-volume assets and established customer relationships; its challenges stem from rivals with a logistical edge in certain locales and the constant threat of weather-driven volume swings, which can sometimes benefit importers who can dump excess salt into the market.

Goderich port expansion – cheaper transportation?

Thesis

Commodity producer, high leverage, management turnover, poor history of capital allocation, and a weak start to the 2025 winter season- a lot has gone wrong, but the future should be different. (Note: I will refer to the winter season that coincides with their fiscal year, Ie, Winter 2025 = Q1 2025 (10/1/24-12/31/24) & Q2 2025 (1/1/25-3/31/25)). In the near term, against the backdrop of an uncertain and volatile market and an especially volatile policy environment, high leverage creates the perfect conditions for Compass’s stock to be sold off.

Cost Reduction – Back to Basics & Debt Refi

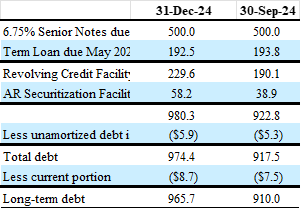

With the recent exit of the fire retardant business, management is now focused on its two core businesses. Capex and R&D will decline, and management’s guidance is for $11m to $13m in cost savings from this move. In a time when Compass needs to preserve liquidity, stemming from $500m of debt due in December 2027 and another $465m due through May 2028. Management stated that they would work to refinance the balance sheet by year-end; however, waiting until the end of 2026 makes more sense, as the incremental time will allow them to generate free cash flow (FCF) and deliver on the cost reduction initiatives, potentially leading to better terms. Recently, S&P downgraded Compass to B due to its leverage profile.

Weak Winters = Weak Volume & Pricing Market – Q2 was an improvement + Working Capital Release

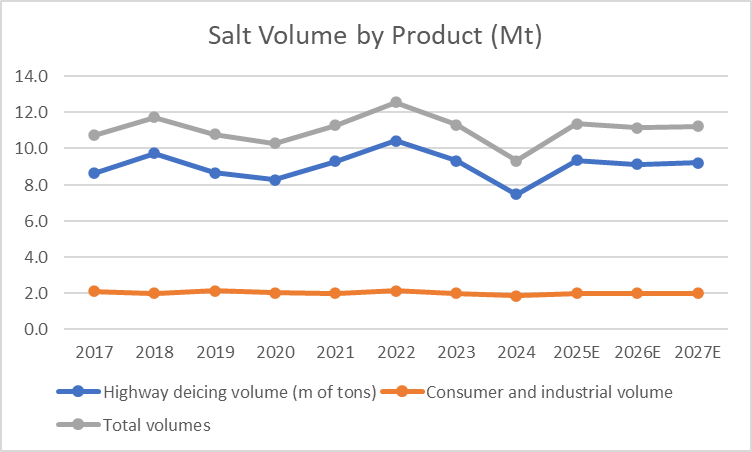

From October to December 2024, the weather was mild, with my estimate of 34 snow days (24-hour periods where snowfall exceeds 1 inch) coming in below historical norms. Compounding this was a weak period from October to December 2023 and a seasonally warmer period from January to March 2024, which resulted in excess salt inventory entering the 2025 winter (October to December 2024 and January to March 2025). Compass reports salt volume in two segments: Highway Deicing (approximately 60% of salt revenue) and Consumer and Industrial (40% of salt revenue). Total salt volumes in 2024 reached 9.3m tons, -17.7% y/y. In Q1 2025, total volumes declined another 12.7% y/y to 2.5m tons. Municipalities typically lock in minimum volume and price contracts prior to the winter season; thus, during periods of excess or shortages of supply, pricing operates with a lag. In Q1 2025, highway pricing declined by 1.2% y/y, a trend that is likely to have continued into the first half of Q2. To manage costs and reduce inventory levels, Compass reduced production at their Goderich mine in 2024, a measure that remained in effect through Q1 2025 and into Q2 2025. This led to significantly higher production costs as fixed costs were spread over a smaller volume. At the end of Q1, inventory stood at $367m, or an estimated 2.9m tons of salt. This will likely be worked down to $270m before increasing again as they ramp up production for the 2026 winter. Inventories are typically at their lowest in Q2 and highest in Q4, just before winter. Additionally, excluding the $35m of receivables from the product recall ($35m liability and $35m A/R expected to be received from insurance), A/R is expected to see a release of approximately $80m throughout 2025. Combining the inventory release + A/R should lead to a $180m tailwind to FCF, aiding their ability to pay off a portion of their debt when they refinance.

Q2 (Jan-March) Let it Snow

Rochester, NY, has now gone six consecutive winters under 100″ of snow. 2022 and 2023 barely reached 50″. That’s the longest streak of sub-100″ seasons since the 1950s. However, Rochester also experienced 43 consecutive days of snowfall (at least 0.1in) in January - February 2025. Salt shortages were prevalent, as competitor American Rock Salt struggled to meet demand. American Rock Salt, one of the most important US producers of road salt, had extra shifts and took additional measures to increase salt supply. This winter through January 2025 ARS shipped over 2.1m tons of salt, compared to 1.8m tons of salt shipped in 2024 for the entirety of the winter season. This should flow through to Compass, given the overlapping markets served. In Q2, I estimate there were 125 snow days in Compass’ 11 core markets, the highest figure in the last several years and closest to Q2 2019’s 122 days, when Compass sold 4.3m tons of highway deicing salt. What’s likely different is the shortage experienced in the northeast.

Large 1-Year Contract to Supply Deicing Salt to Buffalo, NY – Unknown to the Market

Given the proximity to Buffalo, NY, American Rock Salt & Cargill are the primary salt providers for highways. However, due to consecutive days of snow, ARS & Cargill were unable to keep up with demand, allowing Compass to come in as a provider of last resort, and sign a deal.

I am still awaiting confirmation from the Office of the State Comptroller on how these deals are structured. Reports of the contract price are $82/ton compared to the prevailing market price of $69.50 in Q1 25. The original $6m contract was signed on 9/20/24 and subsequently amended to a $56m contract on 2/12/25. Thus, the initial contract had little impact on Q1 25 results; however, a $50m increase in revenue is impactful and would be ~10% -15% incremental to Q2 25 results. I am unsure how often these spending figures are updated, and it’s possible that the contract amount will not fully materialize. This contract value is unlikely to be known by the market, which could be a source of upside to estimates. Reports surrounding the agreement surfaced on 2/6/25.

Estimates Revised Higher + De-leveraging + Cost Reduction + Increased Confidence in Core Business = Undervalued Stock

Compass's premier salt asset will drive positive estimate revisions as cost reductions from the retardant business become apparent and a normalized winter provides a clearer picture of normalized volumes and prices. Several years of mild winters are being extrapolated and assume no operational and financial improvements. Management's back-to-basics mentality is precisely what this company needs. No more side shows. After two years of elevated capital expenditures, 2025 guidance of $80m at the midpoint is approximately $27m below depreciation and amortization (D&A), improving free cash flow (FCF) conversion. Guidance was given before the retardant business closure, driving capex lower. My $73m estimate of capex in 2025 is $27m below $100m of D&A.

Due to the previously mentioned initiatives and events, I am currently well above consensus estimates. In Q3 2026, I expect them to repay $120m of debt and refinance the remaining term loans and debt facilities. Furthermore, declining energy and freight rates throughout Q1 are a tailwind for gross margins. Finally, in November 2024, Reuters reported that Compass was potentially in discussions with private equity to take the company private. Although nothing has materialized, this remains an additional source of upside, particularly in the context of a much cleaner story and reduced capex moving forward. Revenue & Earnings will see a rate of change acceleration in 3 of the next 4 quarters.

Incremental Optionality from Pet Safe Salt

Pet-safe Salt Uses Less Salt: Ice melts typically contain less mined rock salt. Standard Rock Salt Products are nearly 100% sodium chloride and are primarily used for highway deicing and basic bagged rock salt (e.g., Safe Step® 3300). Pet-safe ice melts (e.g., Safe Step and Sure Paws) use a lower percentage of mined NaCl — often less than 50%. Pet-safe salt is usually blended with magnesium chloride, potassium chloride, Calcium magnesium acetate, or Urea. These ingredients are less harsh on paws but more expensive, so rock salt is used sparingly to maintain a balanced cost-to-performance ratio. With increasing dog ownership among younger generations, this will likely increase the demand for pet-safe salt. Compass operates blending facilities, combining mined salt with Magnesium chloride, Potassium chloride, Urea, and CMA (calcium magnesium acetate) (in premium blends). Their facilities often have batching systems and mixers that allow them to control the formulation precisely (e.g., 40% NaCl, 30% MgCl₂, 30% urea). Some blends are coated with anti-caking agents or “pet-safe” surfactants to reduce paw irritation or surface damage. Due to the added complexity, these have higher margins and are more profitable products.

Catalysts

Revenue & Earnings come in well ahead of estimates (Q2 event). Subsequent positive earnings revisions (Q2+).

Free Cash Flow generation de-risks leverage concerns. Debt maturities extended reduce near-term liquidity overhang. (Q2 2025 - Q3 2026 event).

North American plant nutrition segment improves or management exits the business, further simplifying the story and improving earnings power (2025-2026 event).

Potential sale of the business.

Risks

Seasonal Weather Volatility: Sales volumes, particularly in the salt segment, are highly correlated with the severity of winter weather. A colder and snowier winter than average will drive strong demand for deicing salt, often leading to sell-outs and sometimes pricing power as inventories dwindle. Conversely, a mild winter with little snow can crater demand, leaving Compass with excess inventory and forcing it to carry those stocks into the next season or even curtail production temporarily, as it is currently doing. This volatility means the company’s revenues and earnings can swing significantly year to year. Incrementally, the effects of global warming result in significant temperature and seasonal changes from one year to the next, leading me to conclude that Compass’s results and business moving forward will be more volatile than before. As severe winters and warm winters are unpredictable from year to year. This is likely to lead to more shortages and excesses. Lower earnings visibility results in a lower multiple; high operational leverage cuts both ways.

Atlas mine – New mine expected in 2030: Atlas Salt is a pre-operational salt mining development. The company is currently engaged in engineering and permitting processes, with production anticipated to commence in 2030. The strategic focus is directed towards the following geographic markets: Atlantic Canada, Eastern Canada, and the Northeastern United States, resulting in considerable overlap with Compass. Atlas Salt intends to focus on the following market segments: Bulk Commercial, Packaged Commercial, and Packaged Consumer, which competes with Compass's product offerings. The projected production capacity is 2.5m tons of salt per year, with an expected mine lifespan of 34 years, with potential expansion to 4m tons over time. The demand for salt in North America is approximately 70m tons per year. An additional supply of 2.5 to 4m tons in an already balanced market may exert downward pressure on prices and potentially diminish sales volumes for Compass. Atlas expects production costs of $23/mt, compared to Compass in the low $40s. Assuming similar shipping costs of $30/ton, Atlas’s costs are at $53/ton compared to Compass's at $72/ton.

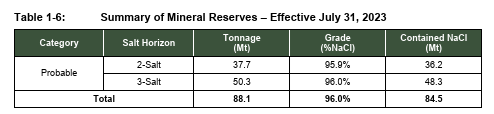

Conversely, this new project provides a valuable comparison for assessing the replacement cost of CMP’s mines. Atlas estimates that the development of a mine containing 1.195b tons of salt (indicated + inferred) or reserves of 84.5mt will require an investment of approximately $480m CAD ($335m USD). In contrast, Goderich possesses around 1.65b tons and a total of 5.8b tons (indicated + inferred). While a direct comparison between Atlas and all of Compass's mines may not be entirely appropriate, the valuation of salt reserves at $0.28 per ton ($335m/1.195B tons) equates to a CMP value of approximately $1.624B, not accounting for the plant nutrition (SOP) business. This valuation contrasts CMP’s current enterprise value (EV) of $1.3B. Startup mines are higher risk than that of Compass, and thus, the potential for cost overruns and delays should result in a premium to the $0.28/ton. Comparing the $335m cost to the 84.5 mt of Salt Mineral reserves equates to $3.96/mt. Compass’s 906mt (accounting for the purity differences) of salt reserves at $3.96/t equates to a value of $3.587B. Discounting Compass’s value by 30% due to higher production costs still yields a value of $1.137B-$2.511B, compared to the $1.3B EV, again excluding the SOP business.

Leverage and Liquidity Constraints: Following the strategic initiatives of recent years, including lithium exploration and acquisitions, as well as weaker operating results, Compass Minerals has taken on a substantial debt load relative to its earnings. Credit rating agencies have downgraded the company’s debt ratings over the past year. Compass may default on its debt if the 2026 and 2027 winter seasons are warmer than normal.

Regulatory and Trade Risks (Tariffs and Trade Policies) + Undifferentiated Product: As a cross-border business with significant operations in Canada, supplying the U.S., and importing some products from outside the U.S., Compass Minerals faces potential changes in trade policies and tariffs. Under NAFTA and now USMCA, salt moves freely between the U.S., Canada, and Mexico without tariffs, which has benefited Compass. However, the heightened tension between Canada and the U.S. could result in tariffs being imposed on salt imports. As a commodity producer, with 73% of its revenue derived from the U.S., countries like Egypt and Chile, where tariffs do not exist, may become more competitive. Deicing salt for the 2025 winter is already in the U.S., posing little to no risk. In 2026, however, if the tariff waffling continues into the summer when purchasing contracts are negotiated, many municipalities may prefer to procure from producers uninvolved in conflicts, opting for firm pricing contracts with domestic or non-tariffed companies.

Additionally, states are implementing “Buy American Salt” policies. In 2023, New York passed a requirement mandating that municipalities must purchase American salt if it is within 10% of foreign contracts. Ohio has a similar policy, where the price must be within 6%. Policies like these require Compass to become increasingly competitive with its pricing, leading to lower prices, increased volume, and narrower margins.

What Would Cause Me To Sell?

The two risks that concern me the most are the new Atlas Mine and the Buy American Salt initiative. If the Atlas Mine comes online sooner than expected, coupled with declines in Compass's profitability, it would indicate a loss of market share. Given the lower production costs at Atlas, I'm worried about the impact on revenue and earnings. If more Buy American Salt initiatives are introduced and American Rock Salt or Cargill announce capacity expansions- likely in anticipation of a continued shift toward this- Compass's results would deteriorate as they either have to lower prices to compete with American companies or face lower volumes.