BGC Q3 Results: Thoughts & What to do

Q3 BGC Results

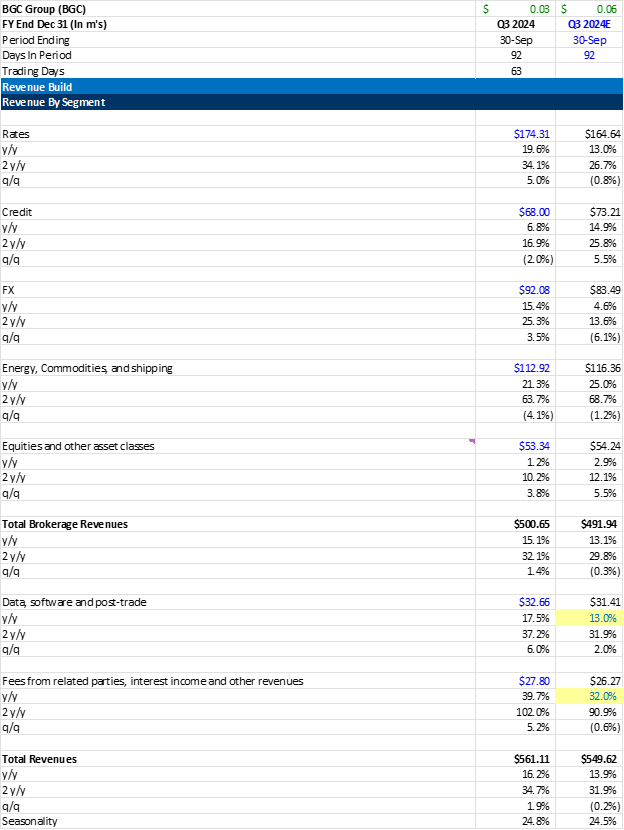

Q3 results were excellent, while the Q4 guidance was slightly below my expectations, even after accounting for the 1-2% contribution from the recently closed Sage Energy Partners acquisition, though this impact is relatively marginal. FX, Rates, and Data performed much better than expected, while ECS and Credit marginally underperformed my estimates.

BGC announced the acquisition of OTC Global and completed the acquisition of Sage Energy Partners (transaction terms have not been disclosed). These additions to BGC's ECS business are immediately accretive and are expected to add $450m+ in revenue, making Energy the largest revenue segment once these deals close. I estimate they paid between 1.5-1.75x sales ($450-$675m). With $450m of revenue and 15% operating margins ($67m), a valuation of 7x-10x EBIT (assuming the business grows similarly to BGC's ECS segment) seems reasonable. I anticipate they may pay more for the OTC Global business due to its hybrid and electronic trading capabilities. Currently, all BGC ECS revenue is voice/hybrid. OTC Global could provide the platform stack needed to transition some of that business to electronic trading, which would result in higher margins and EPS.

FMX Update – They currently have 5 FCMs (Goldman Sachs, JPMorgan, Marex, RBC, and Wells Fargo) trading, and they expect to onboard 5-10 more over the next year, which aligns with the planned launch of Treasury futures in Q1 2025. It’s still early days; although volumes are minimal, this has been the strategy. Year 1 focuses on onboarding as many FCMs as possible, with year 2 ramping up trading activity, and year 3 being the full rollout.

Fully electronic notional volume increased by 17.2% y/y, with total transaction count up 13% y/y. Revenue per dollar of notional (pricing) declined by 4.4% y/y. These trends are positive and show a significant acceleration q/q (Q2 notional: +5.5% y/y, Q2 transaction count: +0.7% y/y, Q2 revenue per dollar of notional: +2.8% y/y). Hybrid results also improved, with notional volumes up 2.1% y/y and transaction count up 8.4% y/y.

Post-Earnings Developments

Following the earnings report, there was mixed news related to CME and positive updates about Howard Lutnick.

CME Update – CME received approval to operate as a broker, allowing trades to be placed directly at the CME's broker and onto their exchange, bypassing traditional FCMs (e.g., JP Morgan, Goldman Sachs, Interactive Brokers). Traditionally, brokers and exchanges remain separate (as demonstrated by issues with FTX). Brokers play a crucial role in the futures market by gathering collateral (e.g., cash) from customers as a form of insurance. This collateral is transferred to the exchange’s clearing house, ensuring that any payment defaults are contained and do not disrupt the broader market. CME’s move to offer brokerage services could reduce costs for traders and may prompt faster onboarding of FCMs, as they may want a contingency plan should CME’s brokerage business gain traction.

Howard Lutnick Update – Howard Lutnick, a key figure in Trump’s circle (co-chair of the Trump transition team), has been involved in identifying and vetting candidates for key positions. This association could explain the recent surge in BGC's stock. It wouldn’t be surprising if Lutnick secures a government role, which could benefit BGC. According to a New York Times article, over the past two years, Lutnick has donated $1 million to Trump’s super PAC, co-hosted a fundraiser at his Bridgehampton, N.Y., home that raised $15 million, and has donated or raised over $75 million for pro-Trump groups this cycle. This connection may bode well for the companies he is associated with

Go Forward

FMX volumes and open interest have recently improved, though nothing is worth writing about. Fenics (both Fenics Markets and Growth Platforms) drives the stock. In addition, integrating the new ECS brokers and the opportunity for margin expansion and growth. While the stock has run post-earnings results, the business continues to perform well and see upside of $17/share over the next 2 years. We continue to own BGC in our portfolios and pound the table until BGC is acquired for a healthy premium (still a few years away).

Hi Dominick, thank you for a write-up.

I have digged a bit deeper in BGC, but their equity-based compensation still puzzles me. It seems to be very dilutive - in Q1 they actually confirmed that stock comps create ~5-6% dilution. In the latest Q3 call they mentioned that they expect shares outstanding to be flat over 2024, even though they've spent $150 mln for share repurchases and $70 mln for redemption and repurchase of equity awards only in the first 6 months of 2024.

So, if we include buybacks which are made just to compensate for dilution, then their profts/FCFs are almost zero. Basically, in line with their reported GAAP profits.

What is your opinion about it?